Battery Storage Capacity: Record Growth and Trends in 2026

Energy storage systems totaled 275.3 GWh in 2025, a 61.3% increase from the previous year, according to the latest report from renewable energy market intelligence provider InfoLink Consulting. In 2026, the world is expected to add another 353.4 GWh of energy storage capacity, driven by demand from artificial intelligence (AI) data centers. The report tracks battery energy storage deployments, cell shipments, and emerging demand from artificial intelligence (AI) data centers.

In 2025, China accounted for the largest share of new battery energy storage capacity, at 167 GWh. The country is expected to add another 203.5 GWh this year according to the report. The United States added 52.1 GWh last year, with 49 GWh of new installations expected in 2026, while Europe installed 25.3 GWh in 2025 and is set to add 35.1 GWh this year. In Australia, 11.4 GWh of new capacity was installed in 2025, with 12.9 GWh projected for 2026. In the Middle East, 8 GWh of new capacity was installed in 2025, while the forecast for 2026 is 20.1 GWh. Significant additions were also recorded in Chile (3.7 GWh) and Japan (2.5 GWh), with expected installations of 6 GWh and 4.2 GWh, respectively, in 2026.

Global shipments of energy storage cells reached 612.39 GWh in 2025, nearly doubling from the previous year, while the forecast for 2026 is 801 GWh, according to InfoLink. Global shipments of battery energy storage systems (BESS) increased by 75.5%, reaching 421.2 GWh in 2025, with 600 GWh projected for 2026. As AI-based data centers consume an increasing share of grid capacity, the role of on-site energy storage is expanding beyond providing an uninterruptible power supply.

Battery systems and data centers can help balance the grid

This means that battery systems deployed alongside data centers are increasingly capable of supporting grid frequency regulation, which could lead to more aggressive investments in storage by energy infrastructure providers for data centers, the consulting firm says.

For its part, the consulting firm Wood Mackenzie noted that long-duration systems accounted for only 6% of global energy storage installations in 2025, as shorter-duration lithium-ion batteries continued to dominate the markets.

“Despite impressive installation growth last year, LDES (Long Duration Energy Storage) technologies are caught in a strategic squeeze,” Jiayue Zheng, managing consultant, energy storage at Wood Mackenzie, recently stated.

LDES technologies are advanced energy storage solutions designed to store electricity for long periods, ranging from several hours to days, weeks, or even months. Unlike conventional batteries (such as lithium-ion), which are efficient for short bursts of energy, LDES technology is essential for balancing power grids based on intermittent renewable sources (sun, wind). “Lithium-ion batteries have captured the economically critical four to eight-hour storage market through superior cost and supply chain advantages, while the LDES lacks sufficient demand and pricing mechanisms to achieve commercial viability.” Wood Mackenzie shows that global funding for LDES fell by 30% in 2025 compared to the previous year, while venture capital investments dropped by 72%. Wood Mackenzie attributed the decline to high interest rates, increasing capital competition from AI data centers and grid infrastructure projects, as well as falling lithium-ion battery prices. “VRFB project costs are projected to fall by over 30% by 2034 but will still be about 240% higher than lithium iron phosphate battery projects for 4-hour duration,” said Priya Shrivastava, research manager, energy storage supply chain at Wood Mackenzie.

Romania is allocating €150 million for the development of storage capacity

Energy Minister Bogdan Ivan announced that Romania will invest €150 million in the development of battery energy storage capacities, under a support scheme financed by the Modernization Fund and aimed at strengthening the national energy system, which has been approved by the European Commission. According to the minister, this scheme will finance the installation of 2,174 MWh of storage capacity. The funding scheme will provide support for up to €69,000 for each MWh of installed storage capacity, with funding per project capped at €15 million, and support covering up to 100% of eligible costs. The call for projects will be launched in the second quarter of 2026, and the investments are expected to be implemented by December 31, 2030.

The dispatchable storage capacity is set to triple this year in Romania, given that nearly 600 MW were installed by the end of 2025, according to ANRE estimates.

The Ministry of Energy notes that Romania has thousands of MW of installed renewable energy capacity, but production depends on the weather; and without batteries, what is produced during the day is often sold cheaply, while in the evening Romania is forced to import energy at higher prices.

The new scheme can help reduce imbalances in the National Energy System and better integrate energy produced by prosumers and from renewable sources, which will have an impact on prices – notes Energy Minister Bogdan Ivan.

“This is Romania’s first scheme under the CISAF. It will help to deploy new electricity storage capacity, which is a key enabler for the large-scale integration of renewable energy into the energy mix. The measure will contribute to a cleaner, more secure and more resilient supply of electricity, in line with the EU’s climate objectives and the Clean Industrial Deal”, said Teresa Ribera, Executive Vice-President for Clean, Just and Competitive Transition.

Romania’s still nascent but rapidly growing battery energy storage industry is preparing to undergo a critical technical evaluation by the transmission and system operator Transelectrica. The company will test its ability to provide a key service for ensuring the safe operation of the national power grid and preventing power outages.

Currently, the largest active standalone energy storage facilities in Romania are those owned and operated by Nova Power&Gas in Floresti (201 MW power, 402 MWh capacity), Sotanga (60 MW, 61 MWh), Doicesti (30 MW, 60 MWh), and Campia Turzii (30 MW, 60 MWh).

As of December 2025, Romania had operational storage systems with a combined installed power of over 494 MW and a total capacity of nearly 914 MWh. This is part of a generation park with a total installed power of approximately 19,400 MW.

A new “largest battery in France” is under construction

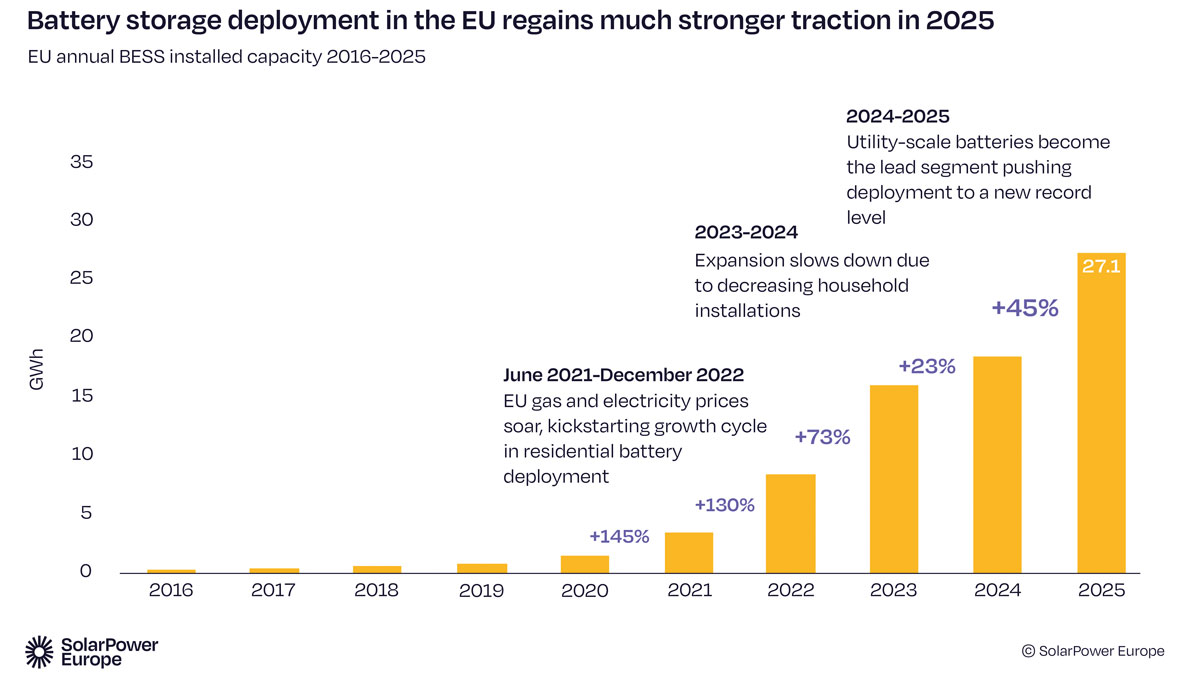

With 27.1 GWh installed in 2025, battery storage has achieved its twelfth consecutive year of record growth in the European Union. While France has announced plans to launch the country’s largest battery, Bulgaria ranks third in the EU in terms of battery storage.

On April 2, Neoen announced the upcoming launch of what will be France’s largest battery, with a capacity of 496 MWh. The battery will be connected to the 400-kV transmission grid. The future Neoen facility will be located approximately 70 km southeast of Paris, in Vernou-la-Celle-sur-Seine (Seine-et-Marne). It will consist of 74 battery containers, spread over an area of 2.4 hectares. The station will have an installed capacity of 248 MW with a storage capacity of 496 MWh, making it the largest battery in France, just ahead of the Cernay-lès-Reims site inaugurated in early 2026 in the Marne department (240 MW/480 MWh).

The future Neoen battery will also be the first to be connected to RTE’s 400-kV power transmission grid, according to the energy company. This battery is designed to meet the grid’s need for flexibility and will provide frequency and voltage regulation services to the grid, helping to relieve congestion in the Île-de-France power grid. This storage project contributes to the transition to low-carbon emissions by promoting the integration of renewable energy capacity.

“Ten years after delivering France’s largest solar farm at Cestas, Neoen is demonstrating that renewable energy generation and large-scale storage are taking their place in the energy mix of our country,” said Guillaume Decaen, CEO of Neoen France. Neoen also clarifies that this project is not receiving any support or subsidies. Construction is scheduled to begin in the summer of 2026, and commissioning is expected in 2028.

It should be noted that the scale of this project remains significantly smaller than that of Neoen’s largest storage facilities, such as the Collie Battery (560 MW/2,240 MWh) located in Australia.

New storage capacities in the EU

An additional 27.1 gigawatt-hours (GWh) of new storage capacity was installed in the European Union in 2025. This represents a 45% increase compared to 2024, a massive figure and a new annual record. Installed capacity now stands at 77.3 GWh, compared to less than 8 GWh at the end of 2021. In four years, European capacity has increased tenfold, according to a report published by Solar Power Europe on January 28, 2026.

Last year, for the first time, large grid-connected batteries accounted for the majority of new capacity, representing 55% of all new batteries. Previously dominated by residential applications, the market is shifting toward large-scale installations.

Why are there so many batteries installed

Solar power will account for nearly 22% of electricity generation in Spain and over 15% in Germany. And to limit the hours with negative prices—which occur 3.4% of the time in Europe—the surplus generation must be absorbed. In addition to flexibility, batteries also help add inertia to the grid. Their growing importance is evident even as the solar market slows down, thanks to public support and lower targets under the PPE3, the European Union’s Third Energy Program.

Residential battery installations (in private homes) fell by 6% to 9.8 GWh. The commercial and industrial segment grew by 31% to 2.3 GWh, but remains marginal, accounting for just 8% of the annual market.

From an industrial perspective, Europe has a potential cell production capacity of 252 GWh, but 92% of that is allocated to electric vehicles. Stationary storage accounts for only 8% of usage.

Leaders in battery storage in the EU

Germany remains in the lead with 6.6 GWh installed, ahead of Italy (4.9 GWh), according to Solar Power Europe. The surprise comes from Bulgaria, in third place with 2.5 GWh, where public subsidies are substantial.

Germany maintained its leading position through record utility-scale installations, resilient growth in C&I, and a more moderate decline in residential deployment.

Italy saw a decline in annual additions, despite steady expansion at the grid scale, due to a sharp drop in residential installations.

Bulgaria experienced a breakthrough year, driven by strong market incentives and support, as well as exceptional progress in large-scale deployment.

The Netherlands ranked fourth thanks to balanced growth across all three segments, driven by improved policies and market conditions.

Spain, in fifth place, implemented BESS on a larger scale, officially recognizing storage as a strategic asset for the energy transition and improving the framework conditions for accelerated deployment.

In total, the top five markets accounted for 63% of the EU’s installed capacity in 2025. In the previous year, nearly 80% was supplied by the five largest markets (DE, IT, SE, AT, NL).

Growth does not guarantee that the European Union’s objectives will be achieved

The significant overall increase in newly installed battery storage capacity (a tenfold increase compared to 2021) does not mean that the targets will be met. The EU would need to repeat this tenfold increase, bringing battery storage to 750 GWh over the next five years. Therefore, while encouraging, current annual deployment levels remain insufficient.

According to SolarPower Europe, the continent has a solid industrial base for battery manufacturing, but its production remains primarily geared toward electric vehicles and does not yet fully meet the needs for large-scale electricity storage.

To strengthen its energy security and competitiveness, Europe must both produce more batteries domestically and accelerate their deployment. This requires the development of local, reliable, and affordable supply chains, as well as high standards of quality and sustainability, to support the development of renewable energy and Europe’s strategic self-sufficiency.

The European battery cell industry is growing rapidly, but uncertainty remains

Although Europe lacks activities related to the extraction and refining of battery minerals, the region has developed a midstream battery industry. However, despite strong production capacities for electrolytes (345 GWheq/a) and separators (220 GWheq/a), production of active materials for cathodes (52 GWheq/a) and anodes (3 GWheq/a) remains very limited. At the cell level, a potential production capacity of 252 GWh has been established through considerable effort, but the industry’s future remains uncertain.

Currently, approximately 92% of existing cell capacity is geared toward serving the electric vehicle market, and 70% consists of nickel-based batteries. This is expected to change in the coming years as demand for stationary storage continues to grow and lithium iron phosphate chemistries dominate the market.

Europe has substantial capacity for assembling packs and modules, with nearly half of all factories located in Germany and less than 20% serving the stationary storage market.

Who dominates the market

China dominates the global battery energy storage market (both production and installation), closely followed by the United States, which is investing heavily in alternatives.

The Asia-Pacific region (China, Japan, South Korea) accounts for the majority of demand, while Australia, Germany, and Italy are major players in residential storage.

The world is entering the Age of Electricity

Energy storage has taken center stage in global innovation, highlighting its increasingly important role in national security and energy systems as the world enters the Age of Electricity. Batteries accounted for 40% of all energy patents in 2023, an unprecedented share for a single technology area—and data shows continued growth between 2024 and 2025.

China, Korea, and Japan remain the primary sources of lithium-ion battery patents, with China’s share rising sharply over the past decade. In solar innovation, patenting has shifted toward perovskite solar cells, which now account for over 70% of solar cell patents by material.

According to the IEA report dated February 18, 2026, China continues to expand its footprint in corporate research and development and patenting, particularly in the fields of energy storage and industrial efficiency, with international patent applications surging in recent years.

Reaching approximately 0.08% of GDP, the intensity of public energy research and development in Europe is approaching the records set in the 1980s and now exceeds that of other major advanced economies. Furthermore, its startup ecosystem has become more dynamic, even as patenting has declined in some major economies.

The United States remains a global leader in venture capital activity, accounting for nearly half of energy venture capital in 2025 and maintaining its strengths across a wide range of technologies.

Japan remains highly specialized in batteries, while also making progress in perovskite solar energy, hydrogen-based fuels and fusion.

Energy storage markets and trends in 2026

China: It dominates the global deployment of battery energy storage systems (BESS), accounting for approximately two-thirds of the world’s installed capacity. Chinese companies such as CATL (the world’s leading manufacturer, with a market share of ~35%) and BYD are at the forefront of production.

United States: One of the largest markets, with widespread adoption of battery storage, particularly in California, where massive systems are in place. Tesla is a major player in the region, alongside Fluence and Sungrow.

Australia: A pioneer in large-scale energy storage, the country continues to develop mega-batteries (such as Neoen and Tesla) to stabilize its grid.

Europe: Germany and France are accelerating their energy storage projects, particularly with players such as TotalEnergies/Saft, Engie, and Neoen.

Germany, one of Europe’s largest electricity markets, is serving as a testing ground for a major agreement. This year, TotalEnergies sold 50% of its stake in a storage portfolio to asset manager AllianzGI.

The industrial aspect is significant: most projects will incorporate batteries supplied by Saft, the group’s French subsidiary. This choice of an integrated development model strengthens control over the value chain. The entry into the market of a leading institutional investor such as AllianzGI illustrates the transition of batteries from a technological innovation to a market infrastructure in a consolidation phase.

France is installing electricity storage batteries, for example in Brittany, to strengthen its grid by mid-2026. Meanwhile, in France, progress is well-documented. According to RTE indicators (battery injection capacity, updated in February 2026), installed capacity has grown from approximately 50 MW in 2019 to nearly 1,600 MW by early 2026.

The Netherlands recorded a record number of energy storage projects in early 2026.

South Africa and Morocco: These African countries are developing projects to secure their power grids amid the growth of renewable energy.

Flexibility: The 2030s mark the transition toward 2050

The European power system’s need for flexibility is growing. According to European Parliament estimates, daily demand could more than double by 2033. By 2050, the Commission estimates that the total flexibility requirement will be approximately 2,189 TWh, or 30% of the EU’s total electricity demand.

Solar photovoltaics are expected to become the main driver of this short-term flexibility need. To support this transition, the Global Commitment on Energy Storage and Grids, adopted at COP29, sets the goal of increasing global storage capacity sixfold by 2030. However, the success of this implementation will depend on the evolution of regulatory frameworks and the implementation of price signals that are attractive to investors.

Storage is entering a phase of large-scale industrial implementation

The implementation of the Electricity Market Design Reform (EMDR), adopted in June 2024, will be a key factor in stabilizing this framework. By combining decentralization and institutional funding, energy storage is emerging as a key driver for a decarbonized and secure European energy mix.

Given that renewable energy will account for 69% of the EU’s energy mix by 2030 (up from 47% in 2024, according to European Commission figures), managing variability is becoming a systemic priority.